Yes, $50k is a Great Start for a Down Payment.

Prove to the Lender,

“You Will Pay Back the Money, They Lend You with Interest”.

First & For Most Proof of Two Year’s Salary in the Same Field of Work!

Good Credit Score, Low Debt Ratio

Lenders look at Your Income: A $50k/year salary, suggests a $125k-$200k

Home Mortgage Approval is generally affordable on that salary,

before considering your Debt-to-Income Ratio (DTI)

Factors Influencing Your Budget:

Your Income: A $50,000 salary usually supports a Home price of $125,000 to $200,000,

depending on debt.

Your Cash: $50,000 could cover a significant down payment

(10-20% on a $250k Home)

Credit Score & Debt: Good Credit & Low Debt (Debt-to-Income Ratio)

Increase Your Borrowing Power.

Calculate Your Debt-to-Income Ratio (DTI)

Calculate Total Monthly Debt Payments:

Add up minimum payments for rent/mortgage, auto loans, student loans, credit cards, and any other recurring debts.

Determine Gross Monthly Income:

Find your total income before taxes and deductions

Divide:

(Total Monthly Debt) / (Gross Monthly Income)

= DTI Ratio (as a percentage).

Example:

If your monthly debts are $2,000 & your gross monthly income is $6,000,

Your DTI is 33% ($2,000 / $6,000)

Loan Type: FHA, VA, or USDA loans offer lower down payments (sometimes 0-3.5%), making homeownership more accessible. (In a Competitive Market Sellers are more apt to accept an offer with more money down)

Key Requirements for Most Lenders:

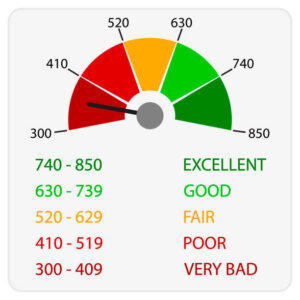

Credit Score:

Aim for 620+, though FHA allows 500 with a higher down payment.

Income & Employment:

Stable job history (often 2+ years) and verifiable income.

Debt-to-Income Ratio (DTI):

Your total monthly debt (including the new mortgage)

Shouldn’t Exceed 43-50% of your gross income.

Down Payment:

Varies by Loan

(Conventional 3-20%, FHA 3.5%, VA/USDA 0%).

Documentation:

Pay stubs, W-2s, bank statements, tax returns, ID.

Connecticut-Specific Programs (CHFA):

Residency:

Must live in CT and occupy the home as your primary residence.

Income Limits:

Your household income must fall within CHFA’s Area Median Income (AMI) limits

First-Time Buyer:

Often required, or haven’t owned in 3 years, or buying in a targeted area.

Property Type:

Owner-occupied 1-4 unit homes, condos, townhouses.

🗝 Steps to Take:

Check Your Credit: Know Your Score & Address Any Issues.

Free Credit Report: https://www.experian.com/

Gather Documents: Collect Pay Stubs, Tax Forms, Bank Statements.

Talk to a Lender: Determine How Much You Can Afford,

Including Closing Costs.

Get Pre-Approved: Crucial for Making Offers!

Sellers Will Not Look at Offers With Out a Pre-Approval Letter.

Buzz The 🐝 860.927.1819